Finance is a big word we as adults often cringe from. We are constantly being nagged with the idea of having to save for future needs, emergency funds, and other bills and utilities we need to pay. It is therefore important that you keep your finances straight and always watch your expenses.

Read MoreThe construction industry in Canada is booming, employing well over 1.4 million people and is solely responsible for roughly $150 billion back to the economy each year. Suffice to say, there’s a lot of value of industry to do with construction, and the construction industry is only expected to grow steadily over the next few years. In order to ensure quality of work and to guarantee that deadlines can be met and projects can be completed on time, most contractors and construction companies are being required to have some degree of performance security. Typically, that comes in the form of a surety bond.

What is a surety bond, you might ask?

What is a surety bond?

As a subcontractor or even a general contractor, you may be asked to secure a surety bond or “surety insurance” by one of your prospect or existing clients. If you work on a public project or a government mandated project, you may be required to purchase a surety bond.

A surety bond is like insurance, except not. It involves three parties, not just two. Those parties are the business (the principal), the surety (the one issuing the bond), and your client (the obligee.) The surety bond will be paid out to the client, not to the business (this is insurance protecting your client and not you) and, at the tail-end of the bond’s duration, you’ll be expected to pay back the entirety of the surety bond to your surety provider.

Why have a surety bond?

Note that there are different types of surety bonds. There are contract surety bonds, commercial surety bonds, and court surety bonds. Contract surety bonds are in-place to guarantee that the obligations of a construction project/contract can be met. Commercial surety bonds are guaranteed to ensure compliance to all the required codes, such as if your company requires a particular license to operate. Finally, a court surety bond is designed to help cover losses should there be a court proceeding.

A contract surety is the most likely bond to be required in the construction or manufacturing industry. With this type of surety coverage, any consequential costs or remaining costs that may arise from a contract where your business is unable to fulfill the full terms of its terms and conditions is covered by the surety bond. The client can use the money they receive to complete the project and/or significantly mitigate their financial losses. Contract surety bonds often come in the form of:

- Labour and Material Payment – This bond guarantees that the principal (business owner) will pay all its suppliers and subcontractors

- Performance Bond – This bond guarantees that the principal (business owner) will complete their end of the contract, including all obligations and fulfillments.

There are also bonds you may acquire for contract acquisition, i.e. bid bonds. These show a potential client that you are qualified for a contract and may put you ahead of other bidders when it comes to the final decision process about which contractor to choose.

Do I need to have a surety bond?

Typically, if you work in the construction and/or manufacturing industry, the answer is yes: you need a surety bond. Contractors are often required to purchase bonds, as their clients may require it, or government parties may need it. Private clients can stipulate that all their contractors have bonds.

Furthermore, having bonds for the tendering stage can make you appear as a more reputable candidate. Bonds are designed to protect the clients, so while you may hesitate on this front due to the fact that it’s not insurance for you, it’s highly necessary for your reputation and perhaps to even acquire work at all. Construction workers, manufacturers, suppliers, and other types of contractors may require the purchase of surety bonds.

How much does a surety bond cost?

Calculating a surety bond is a little different than calculating insurance costs. It depends on the provider you go with, for one, as there are different cost structures. You’ll typically pay between 1-15% of the total coverage that is provided by the bond. The riskier you are, the more you’ll pay.

Bond rates may be determined by the type of bond, length of the bond obligation, your risk level (including personal demographics like business revenue, experience, licenses, financial history, credit score, and so forth) and the overall value of the bond.

Talk with a surety bond provider or broker if you aren’t sure!

Read More

Below are summaries of some basic principles you should understand when evaluating an investment opportunity or making an investment decision. Rest assured, this is not rocket science. In fact, you’ll see that the most important principle on which to base your investment education is simply good common sense.You’ve decided to start investing. If you’ve had little or no experience, you’re probably apprehensive about how to begin. Even after you’ve found a trusted financial advisor, it’s wise to educate yourself, so you can evaluate his or her advice and ask good questions. The better you understand the advice you get, the more comfortable you will be with the course you’ve chosen.

Below are summaries of some basic principles you should understand when evaluating an investment opportunity or making an investment decision. Rest assured, this is not rocket science. In fact, you’ll see that the most important principle on which to base your investment education is simply good common sense.You’ve decided to start investing. If you’ve had little or no experience, you’re probably apprehensive about how to begin. Even after you’ve found a trusted financial advisor, it’s wise to educate yourself, so you can evaluate his or her advice and ask good questions. The better you understand the advice you get, the more comfortable you will be with the course you’ve chosen.

Making investment decisions based on emotions and not on facts

Making investment decisions based on emotions and not on facts 1.There’s no better day than today.

1.There’s no better day than today. 2. Talk with the pro’s.

2. Talk with the pro’s. 3. Be a regular consumer.

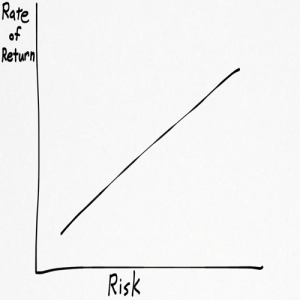

3. Be a regular consumer. 4. Take a risk.

4. Take a risk.